Tax experts also caution that the Income Tax Department's e-filing portal often witnesses heavy traffic close to the deadline, increasing the chances of technical glitches and delayed submissions. Late Filing Can Cost You Up to Rs.5,000

Under the Income Tax Department's rules, taxpayers who fail to file their returns within the prescribed due date will be required to pay a late filing fee.

- Taxable income above Rs.5 lakh: Late fee of up to Rs.5,000

- Taxable income up to Rs.5 lakh: Late fee of Rs.1,000

Filing your return on time can help you avoid these additional costs and ensure faster processing of refunds.

How to File Your Income Tax ReturnTaxpayers can complete the filing process online by following these simple steps:

- Log in to the Income Tax Department's e-Filing portal.

- Select the appropriate ITR form.

- Review the pre-filled personal and financial information.

- Enter details of your income, deductions, and exemptions.

- Verify the tax computation.

- Submit the return and complete verification using Aadhaar OTP or an Electronic Verification Code (EVC).

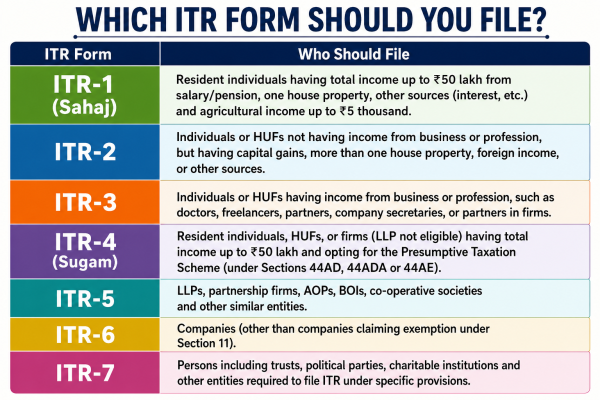

Selecting the right ITR form is just as important as filing on time. The applicable form depends on factors such as:

- Nature and source of income

- Total annual income

- Category of taxpayer (individual, business owner, professional, etc.)

Submitting an incorrect ITR form may result in your return being treated as defective or invalid, requiring you to file it again.

Who Needs to File by July 31?

The Income Tax Department has already enabled online and offline utilities for ITR-1 to ITR-4 on the e-filing portal.

The July 31, 2026 deadline generally applies to:

- Salaried employees

- Pensioners

- Individual taxpayers with relatively simple income sources

Other Filing Deadlines

Not all taxpayers have the same due date.

- August 31, 2026: Taxpayers with business or professional income whose accounts are not required to be audited (including eligible ITR-3 and ITR-4 filers).

- October 31, 2026: Businesses, firms, and companies whose accounts are required to be audited under the Income Tax Act.

Taxpayers should check the applicable deadline based on their filing category.

What Happens If You File Late?Apart from the late filing fee, delayed ITR submission can lead to several inconveniences, including:

- Interest on outstanding tax liability

- Delay in receiving income tax refunds

- Loss of the ability to carry forward certain eligible losses to future assessment years

- Complications while applying for bank loans, visas, or submitting financial documents that require proof of income

Filing your ITR well before the deadline not only helps you avoid penalties but also reduces the risk of portal-related issues and gives you enough time to correct any errors.

-

Ayatollah Khamenei: Legacy of resistance more alive than before

-

Rajasthan: 3 men tortured, forced to chant Jai Shri Ram

-

Madhuri Jain is richest; reported net worth of Lock Upp 2 stars

-

Ninjacart Nets $6 Mn From Accel, Nandan Nilekani; Eyes IPO In 2 Years

-

Karnataka: Seven workers killed after boulder collapses at stone quarry near Bengaluru