The Employees' Provident Fund (EPF) is one of India's most important retirement savings schemes, designed to provide financial security after retirement. However, many employees often wonder whether they can withdraw their entire Provident Fund balance whenever they need money. The question has become even more relevant with discussions around EPFO 3.0 and upcoming digital service upgrades.

The simple answer is no. Under the current rules of the Employees' Provident Fund Organisation (EPFO), members cannot withdraw their full PF balance while they are actively employed. Complete withdrawal is permitted only under specific circumstances, while partial withdrawals are allowed for certain approved purposes.

Here's a detailed look at the latest EPF withdrawal rules and when you can access your savings.

Can You Withdraw 100% of Your EPF Balance?

EPFO permits complete withdrawal of your Provident Fund only in limited situations.

If you are currently employed, you cannot withdraw your entire EPF corpus simply because you want access to the money. The fund is intended to serve as long-term retirement savings and is therefore protected by withdrawal restrictions.

According to EPFO rules, full withdrawal is generally allowed only in the following situations.

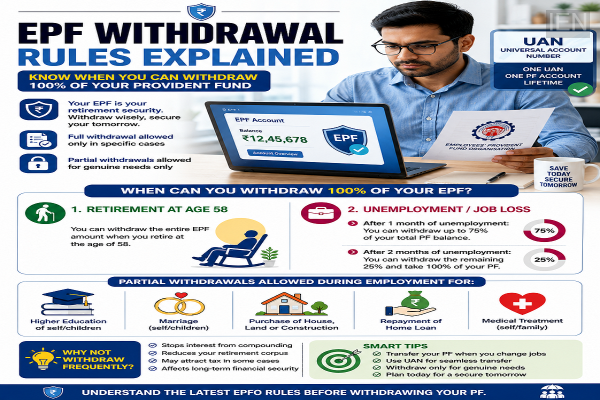

1. Full Withdrawal After Retirement

Employees become eligible for final settlement of their EPF account after attaining the prescribed retirement age of 58 years.

Once eligible, members can apply for final settlement and withdraw the entire accumulated balance, including employee contributions, employer contributions, and applicable interest, subject to EPFO rules.

2. Full Withdrawal After Prolonged Unemployment

Employees who lose their jobs can also access their EPF savings under certain conditions.

The withdrawal rules are divided into two stages:

After One Month of Unemployment

If an EPF member remains unemployed for one month, they can withdraw up to 75% of the total PF balance.

After Two Months of Unemployment

If unemployment continues for two months or more, the member becomes eligible to withdraw the remaining 25%, effectively allowing withdrawal of the full EPF balance.

This provision is intended to provide financial support during periods without employment.

Should You Withdraw PF After Changing Jobs?

Many employees mistakenly believe they should withdraw their PF balance whenever they switch employers.

However, EPFO strongly recommends transferring the accumulated balance to the new employer instead of withdrawing it.

The transfer process can be completed using the employee's Universal Account Number (UAN), allowing the PF account to continue seamlessly with the new organization.

Why Transferring Your PF Is Better

Keeping your EPF account active through transfer offers several long-term benefits.

Continued Interest Earnings

Your accumulated balance continues to earn annual EPF interest, helping your retirement corpus grow over time.

Uninterrupted Service History

PF transfer maintains continuous employment records, which can be beneficial for various retirement-related calculations and future benefits.

Potential Tax Savings

Frequent withdrawals after changing jobs may reduce your retirement savings and, in certain situations, could also have tax implications depending on applicable income tax provisions.

Partial Withdrawal Is Allowed During Employment

Although complete withdrawal is restricted while you remain employed, EPFO permits partial withdrawals, commonly known as EPF advances, for several specified purposes.

Eligible reasons include:

-

Higher education.

-

Marriage of self or children.

-

Purchase of a house or residential plot.

-

Construction of a home.

-

Repayment of a home loan.

-

Medical treatment for self or eligible family members.

Each category has separate eligibility conditions, including minimum years of service, withdrawal limits, and documentation requirements.

Things to Consider Before Withdrawing PF

While withdrawing PF can provide immediate financial relief during emergencies, it may significantly reduce your retirement savings.

The EPF scheme offers several long-term advantages, including:

-

Mandatory monthly savings.

-

Employer contributions.

-

Annual interest credited to the account.

-

Tax benefits under applicable provisions.

-

Financial security after retirement.

Withdrawing funds frequently can reduce the compounding benefits that make EPF an effective long-term wealth creation tool.

Reserve PF for Genuine Emergencies

Financial experts generally advise employees to avoid withdrawing their Provident Fund unless absolutely necessary.

For those changing jobs, transferring the EPF account rather than withdrawing the balance helps preserve retirement wealth while ensuring uninterrupted interest accumulation.

Using partial withdrawals only for genuine emergencies or approved purposes can help maintain a strong retirement corpus.

Key Takeaway

Under current EPFO rules, employees cannot withdraw their entire Provident Fund balance while they are actively employed. Full withdrawal is generally permitted only after retirement at 58 years of age or after two months of continuous unemployment, with up to 75% withdrawal allowed after one month without a job. Employees changing jobs are advised to transfer their PF using their UAN instead of withdrawing the balance, while partial withdrawals remain available for approved purposes such as education, marriage, home purchase, home loan repayment, and medical emergencies. Preserving your EPF savings can significantly strengthen your financial security during retirement.

-

United States strikes Iran after cargo ship attack

-

BPSSC Home Guard Recruitment: Recruitment for Company Commander posts in Bihar Home Guard; applications begin on June 30..

-

MPSC Group C Recruitment 2026: Apply for 2,619 Group-C posts in Maharashtra; an opportunity for graduates..

-

CBSE Language Policy Update: Students Can Continue with Current Language Choices

-

Chhattisgarh Pre-DElEd 2026 Results Announced: Check Your Scores Now