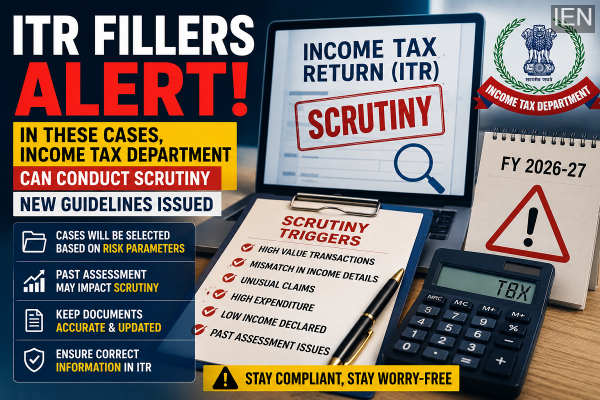

The Income Tax Department has released fresh guidelines for selecting Income Tax Returns (ITRs) for compulsory scrutiny during the financial year 2026-27. The new framework, issued by the Central Board of Direct Taxes (CBDT), outlines the categories of taxpayers and transactions that may attract detailed examination by tax authorities.

The updated rules will apply to income tax returns filed for the financial year 2025-26 and are aimed at strengthening tax compliance, improving transparency, and identifying cases where discrepancies or potential tax risks may exist.

While the announcement has sparked concerns among taxpayers, experts say that individuals who accurately disclose their income and maintain proper financial records should not be worried. However, understanding the scrutiny process and the situations that may trigger an investigation is important for every taxpayer.

What Is Income Tax Scrutiny?

Income tax scrutiny is a detailed review conducted by the Income Tax Department to verify the information provided in a taxpayer's return.

During this process, tax officials may examine:

-

Income declared in the return

-

Investments and financial assets

-

Tax deductions and exemptions claimed

-

Bank account transactions

-

Capital gains and other sources of income

-

Supporting documents and financial records

The purpose of scrutiny is to ensure that the information reported by the taxpayer is accurate and consistent with available financial data.

If any mismatch, unusual transaction, or risk indicator is identified, the return may be selected for detailed verification.

CBDT Releases New Scrutiny Selection Guidelines

Under the latest instructions, certain categories of returns will be compulsorily selected for complete scrutiny based on predefined risk parameters.

The Income Tax Department uses data analytics, information received from financial institutions, and other compliance tools to identify cases that may require closer examination.

Returns showing unusual patterns, inconsistencies, or potential underreporting of income could fall within the scrutiny net.

The department's objective is not only to detect tax evasion but also to improve voluntary compliance among taxpayers.

High-Risk Cases Could Face Mandatory Examination

According to the new framework, taxpayers whose returns trigger specific risk indicators may be selected for detailed scrutiny.

These risk indicators may include:

-

Significant mismatch between reported income and financial transactions

-

Large-value investments not supported by declared income

-

Unusual deduction or exemption claims

-

Inconsistencies between tax returns and information available with the department

-

Cases identified through risk assessment systems

Taxpayers selected under these parameters may be asked to submit additional documents, clarifications, and supporting evidence to justify the information provided in their returns.

Previous Tax Assessments May Influence Future Scrutiny

One of the key points highlighted by tax experts is that earlier assessment outcomes can impact future scrutiny decisions.

If a taxpayer's income was increased during a previous assessment because the tax officer found discrepancies in the return, that history could become a factor when selecting subsequent returns for examination.

In other words, taxpayers who have faced additions to taxable income in past assessments may be more likely to attract attention in future years.

This makes accurate reporting and compliance even more important for individuals and businesses.

No Major Changes for Honest Taxpayers

Despite concerns over the new guidelines, tax professionals believe that the overall framework remains largely similar to previous years.

There are no sweeping changes that significantly alter the scrutiny selection process for ordinary taxpayers.

Individuals who:

-

File returns on time

-

Report income accurately

-

Maintain proper documentation

-

Avoid incorrect deduction claims

are unlikely to face unnecessary difficulties.

The guidelines are primarily designed to target high-risk and non-compliant cases rather than routine taxpayers.

How Taxpayers Can Avoid Problems During Scrutiny

Experts advise taxpayers to maintain complete and updated financial records throughout the year.

Important documents that should be preserved include:

-

Form 16 and salary records

-

Bank statements

-

Investment proofs

-

Capital gains statements

-

Loan and interest certificates

-

Property transaction documents

-

Tax-saving investment records

Before filing an ITR, taxpayers should also cross-check their information with Form 26AS, AIS (Annual Information Statement), and other official tax records to ensure there are no mismatches.

Key Precautions Before Filing Your ITR

To minimize the chances of scrutiny-related issues, taxpayers should:

-

Report all sources of income accurately.

-

Verify financial data with AIS and Form 26AS.

-

Avoid making unsupported deduction claims.

-

Keep records of major transactions and investments.

-

Respond promptly to any tax notices received.

-

Ensure consistency between declared income and spending patterns.

The Bottom Line

The CBDT's latest scrutiny guidelines for FY 2026-27 reinforce the government's focus on data-driven tax compliance. While the Income Tax Department will continue to monitor high-risk returns closely, taxpayers who file accurate returns and maintain proper documentation have little reason to be concerned.

As the ITR filing season progresses, transparency, accurate disclosures, and proper record-keeping remain the best safeguards against scrutiny-related complications.

-

Post Office vs SBI RD: Where Will ₹10,000 Monthly Investment Earn More After 5 Years?

-

EPFO’s Free Insurance Benefit Explained: How Employees Can Get Up to ₹7 Lakh Cover Without Paying Any Premium

-

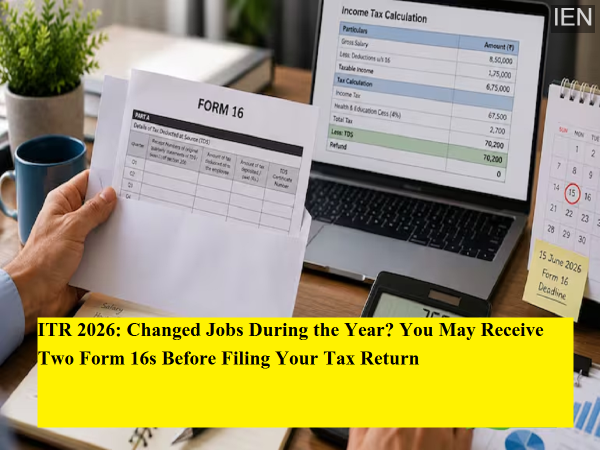

ITR 2026: Changed Jobs During the Year? You May Receive Two Form 16s Before Filing Your Tax Return

-

Grammy-Winning Songwriter Talay Riley, 35, Stabbed To Death In London

-

Kangana Ranaut Honours Odisha's Iconic Kotpad Saree During Bhubaneswar Visit: Know More About Her Handloom