Tax Benefits, Returns, Lock-In Rules and the New NPS Retirement Income Scheme Explained

Retirement planning is one of the most important financial goals for both salaried professionals and business owners. Building a large retirement corpus requires disciplined investing over decades, and two of the most popular options in India are the National Pension System (NPS) and Mutual Funds.

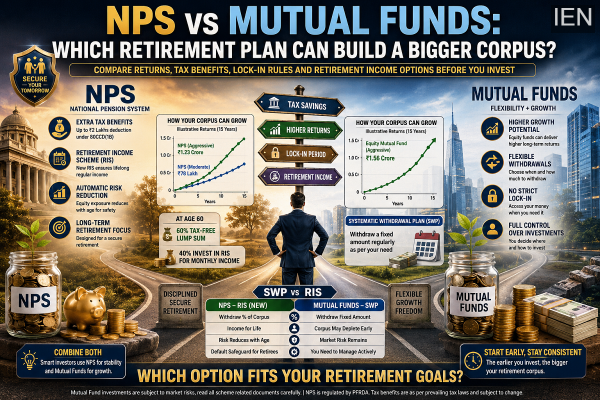

For years, mutual fund investors have relied on Systematic Withdrawal Plans (SWPs) to generate regular income after retirement. However, a major development in 2026 has changed the conversation. The Pension Fund Regulatory and Development Authority (PFRDA) has introduced the new Retirement Income Scheme (RIS) within NPS, creating a fresh debate over which retirement vehicle now offers a better balance of growth, security, and income.

Here's a detailed comparison of NPS and Mutual Funds based on returns, taxation, flexibility, and retirement income potential.

Returns: High Growth vs Built-In Risk Management

Mutual Funds

For investors seeking maximum long-term wealth creation, equity mutual funds have traditionally been the preferred choice.

Historically, diversified equity funds have offered the potential to generate annualized returns in the range of 12% to 15% over long investment horizons, although actual returns vary based on market performance.

Advantages include:

-

Higher growth potential

-

Inflation-beating returns

-

Flexibility in fund selection

-

Full market participation

However, there is also greater exposure to stock market volatility. If markets decline significantly near retirement, the value of the accumulated corpus can be affected.

NPS and the New Retirement Income Scheme

NPS follows a more structured approach to retirement investing.

Under the newly introduced Retirement Income Scheme (RIS), the portfolio gradually becomes more conservative as the investor ages.

For example:

-

Equity allocation may remain higher during younger years.

-

Around age 60, equity exposure may be limited to approximately 35%.

-

By age 75, equity exposure can gradually reduce further while debt and government securities become dominant.

This automatic risk reduction is designed to protect retirement savings from sharp market fluctuations during later years of life.

Tax Benefits: NPS Holds a Clear Edge

Mutual Funds

Mutual funds offer investment flexibility but do not provide the same level of dedicated retirement-related tax benefits.

Taxation depends on:

-

Holding period

-

Fund category

-

Applicable capital gains rules

Investors may pay:

-

Short-Term Capital Gains (STCG) tax on short holding periods

-

Long-Term Capital Gains (LTCG) tax on qualifying long-term gains

While tax-efficient in certain situations, mutual funds generally do not offer the same upfront deductions available under NPS.

NPS

NPS remains one of India's most tax-efficient retirement products.

Key tax benefits include:

-

Deduction up to ₹1.5 lakh under Section 80C

-

Additional deduction up to ₹50,000 under Section 80CCD(1B)

-

Tax benefits on employer contributions, where applicable

-

Up to 60% lump-sum withdrawal at retirement can be tax-free under prevailing rules

These advantages make NPS particularly attractive for individuals looking to reduce taxable income while building retirement savings.

Lock-In and Flexibility

Mutual Funds

Flexibility is one of the biggest strengths of mutual funds.

Investors can:

-

Start or stop SIPs anytime

-

Switch between funds

-

Redeem investments when required

-

Access funds for emergencies

Except for certain tax-saving funds, most mutual fund schemes do not impose strict lock-in requirements.

This makes them highly suitable for investors who value liquidity and financial flexibility.

NPS

NPS is specifically designed for retirement.

As a result:

-

Funds remain largely locked in until retirement age.

-

Withdrawals are governed by specific regulations.

-

Partial withdrawals are allowed only under certain conditions.

While this lack of flexibility may seem restrictive, it also helps investors maintain discipline and avoid prematurely spending retirement savings.

Retirement Income: SWP vs RIS

The most interesting comparison today is between the traditional Mutual Fund SWP strategy and the newly launched NPS Retirement Income Scheme.

Mutual Fund SWP

A Systematic Withdrawal Plan allows investors to decide exactly how much money they wish to withdraw periodically.

Benefits include:

-

Complete withdrawal flexibility

-

Control over cash flow

-

Ability to modify withdrawals at any time

However, there is a risk.

If withdrawals are too aggressive during weak market periods, the retirement corpus may deplete faster than expected.

NPS Retirement Income Scheme (RIS)

The new RIS model aims to provide a more structured retirement income solution.

Instead of withdrawing arbitrary amounts, retirees receive income linked to a systematic percentage of the retirement corpus.

Potential advantages include:

-

Better longevity of retirement savings

-

Automatic risk reduction with age

-

Reduced portfolio management burden

-

More predictable retirement income planning

Financial experts believe this feature could be particularly valuable for retirees who depend heavily on their retirement corpus for regular income.

Which Option Is Better for You?

NPS May Be Suitable If:

-

Retirement is your primary financial goal.

-

You want maximum tax benefits.

-

You prefer disciplined long-term investing.

-

You do not have alternative pension or rental income.

-

You want a structured post-retirement income stream.

Mutual Funds May Be Suitable If:

-

You want maximum investment flexibility.

-

You can manage market volatility.

-

You have other income sources after retirement.

-

You prefer controlling withdrawals yourself.

-

You are comfortable taking a higher equity allocation for potentially higher returns.

The Smart Approach: Use Both

Many financial planners believe the NPS versus Mutual Fund debate does not require choosing only one option.

A combination strategy can often work best:

-

Use NPS for retirement discipline and tax savings.

-

Use mutual funds for growth and liquidity.

-

Create multiple income sources for retirement.

This diversified approach can provide both wealth creation during working years and income stability after retirement.

The Bottom Line

The introduction of the NPS Retirement Income Scheme has strengthened NPS as a retirement-focused product. It now offers a more structured approach to generating income after retirement while automatically reducing investment risk with age.

However, mutual funds continue to excel in terms of flexibility, liquidity, and long-term growth potential. Investors who are comfortable managing their portfolios may still find mutual funds highly attractive.

Ultimately, the better option depends on individual financial goals, risk tolerance, tax considerations, and retirement income requirements. For many investors, combining both NPS and mutual funds may offer the most balanced path toward a financially secure retirement.

Disclaimer: Investments in market-linked products are subject to market risks. Investors should evaluate their financial objectives and consult a qualified financial advisor before making investment decisions.

-

Indian Men's Hockey Team Falls Short Against Netherlands in Close Match

-

DG Shipping directs firms to restrict deployment of Indian seafarers in Gulf zone

-

Meet Swara Jadhav: The 13-Year-Old Spinner Taking Mumbai Cricket by Storm

-

Tu Hi Re Dil Mein actor Abrar Qazi gets candid about his role; says 'Playing a good character is tough since one has to bring authenticity'

-

Viswanathan Anand's son Sai Akhil Anand showcases art inspired by nature in Bengaluru