MobiKwik’s Q4 results at the tail end of last week brought up some interesting views over this past week, but our reading of the numbers raised a deceptively simple question: If payments GMV is growing 58% and UPI transactions are exploding 170%, why has payments revenue barely moved for over a year?

This contradiction sits at the centre of the company’s entire story and could define the future for MobiKwik, which has painfully pieced together its fintech empire in the past year and a half.

On the surface, the quarter looked reassuring for the Delhi NCR-based giant. For instance, it turned EBITDA positive and PAT also recovered some momentum. As lending margins improved, management sounded far more confident than it did during FY25’s regulatory disruptions.

MobiKwik increasingly appears to be moving away from being a payments company and toward becoming a regulated lending and merchant-finance platform. Its recent acquisition of an NBFC licence is a key piece in this.

The problem is that the transition is still incomplete, while the economics of the legacy payments business continue weakening, there is a top-of-the-funnel threat for MobiKwik.

After a difficult FY25 marked by regulatory disruptions in its lending business and heavy losses, MobiKwik is showing signs of operational turnaround. The fintech company reported a consolidated net profit of ₹4.4 Cr in the March quarter, compared to a loss of ₹56 Cr a year earlier, while EBITDA also turned positive at ₹17.4 Cr.

While revenue growth remained modest at 7.8% YoY, the company managed to significantly improve profitability across both its payments and financial services businesses, signalling that the worst phase of stress following the RBI’s BNPL and FLDG-related changes may now be behind it.

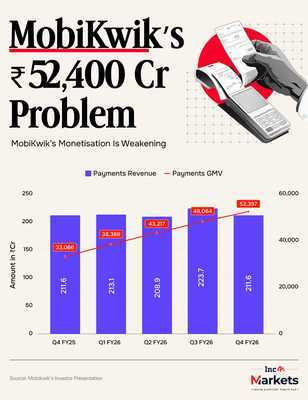

Mobikwik’s Payment Revenue ConundrumHowever, the number that stands out most in the quarter is payments revenue. In Q4 FY26, it came in at ₹211.6 Cr, exactly the same as Q4 FY25. The increase in volumes has not moved the payments revenue needle by much.

At this stage, that looks less like a temporary issue and more like a structural characteristic of the business, which is heavily reliant on UPI.

The company’s payment take rate also fell from 64 bps in Q4 FY25 to 40 bps in Q4 FY26, a 37% decline in yield in one year. Compared to FY24’s 83 bps, monetisation per rupee of GMV has effectively halved over two years.

Importantly, management also acknowledged during the earnings call that monetisation pressure is not limited to UPI alone. The company admitted that take rates in some legacy businesses have also moderated.

That matters because it suggests the issue may not simply be temporary UPI revenue dilution, but broader structural compression across the payments stack itself. What remains clear is that the bulk of transaction growth is coming from UPI, where MDR remains zero. Every additional UPI transaction increases GMV but pushes blended revenue yield lower.

Mobikwik’s thesis is that UPI users eventually move into wallets, bill payments, lending and merchant products over time. That may happen, but it remains a longer-term monetisation argument rather than evidence visible in current-quarter numbers.

“There is more UPI mix in the overall payment GMV, due to which we have so far not been able to demonstrate significant revenue growth. But we have invested and we will be delivering growth in the coming days and quarters,” Mobikwik CFO Upasana Taku said, without giving any further details in the post-earnings call.

In effect, the company is no longer treating UPI as a monetisable product by itself. Instead, UPI increasingly functions as a customer acquisition and engagement rail through which MobiKwik hopes to monetise downstream products such as lending, merchant payments, bill payments and financial distribution.

Where the company does deserve credit is on payments gross margin expansion. Gross margin rose from 23.9% in Q4 FY25 to 39.1% in Q4 FY26, while gross profit increased 64% YoY despite flat revenue.

The gains were driven by lower gateway costs, which declined from ₹147.1 Cr to ₹119.3 Cr, down 19% YoY, alongside lower user incentives, which fell from ₹14 Cr to ₹9.6 Cr, down 32% YoY.

However, the problem is that the scope for further compression now looks limited. Gateway costs as a percentage of GMV have already dropped from 44 bps in Q4 FY25 to 23 bps in Q4 FY26. User incentive costs are down to just 2 bps of GMV, effectively negligible.

Payments GMV grew 58% YoY to ₹524 Bn in Q4 and 57% for the full year to ₹1,821 Bn. UPI transactions rose 170% YoY, with the company claiming to be the second-fastest in India in terms of UPI growth numbers.

But take rates have already fallen sequentially from 47 bps in Q3 to 40 bps in Q4, while cost reductions are nearing exhaustion. Net payments margin stood at 16 bps in Q4 and is likely close to the upper end achievable under the present mix. revenue moved from ₹213.1 Cr to ₹208.9 Cr to ₹223.7 Cr to ₹211.6 Cr. For five straight quarters, the business has stayed trapped within a narrow ₹208.9-223.7 Cr range.

Financial Services: A Long Way From PeakFinancial services, which is primarily the lending business, was clearly the strongest part of the quarter. The gross margin progression over the past five quarters is commendable, growing 4% to 13% to 42% to 57% to 59% in the quarter under review.

The share of Super Prime borrowers have also increased from under 10% to 32%, delinquency trends improved across all origination cohorts with roughly 35% lower risk versus peak stress levels, and repeat borrower contribution rose from 20% to 63.5%.

While the 19x YoY increase in gross profit was notable, Q4 FY25 was an exceptionally weak quarter, with gross margin collapsing to 4% during the FLDG and BNPL regulatory disruption.

The better indicator is the sequential recovery since Q2 FY26, where margins improved from 42% to 57% to 59%. That progression aligns with improving borrower quality.

The net margin in this vertical also improved to 5.39% in Q4 from 0.35% a year earlier, while margins improved sequentially through every quarter of FY26.

For a business that faced severe disruption after the RBI’s BNPL restrictions and FLDG cap in FY25, the speed of recovery has been faster.

There is, however, an important caveat. Financial services GMV declined 7% QoQ in Q4, from ₹900 Cr to ₹837.7 Cr.

Per company, it is a deliberate strategy to prioritise profitability over volume, but it also means lending volumes are not currently growing in absolute terms.

Full-year FY26 disbursals stood at ₹3,238 Cr, up 31% over FY25’s depressed levels, but still below FY24 levels when the business operated at significantly larger scale and with a broader product mix.

The company has materially reduced the size of its lending operations from peak levels, which also has to be seen how far the recovery still has to go. Notably, financial services revenue for FY26 was ₹261.9 Cr, compared to ₹557.9 Cr in FY24.

Why MobiKwik’s NBFC Ambition Is A Big DealThe most important development in the quarter may not actually be visible in current earnings numbers at all. It is the company’s attempt to evolve beyond being merely a payments intermediary and into a regulated lending infrastructure platform.

Last month, the company secured a NBFC licence from the Reserve Bank of India (RBI), over one year after incorporating a wholly owned subsidiary, MobiKwik Financial Services Private Limited.

According to fintech analysts, regulatory positioning itself is becoming a competitive moat in Indian fintech. Many players have distribution. Far fewer possess meaningful lending architecture or regulatory flexibility. That is where MobiKwik may hold an underappreciated strategic advantage.

Unlike several fintech peers that remain dependent on pure lending service provider models, MobiKwik’s NBFC ambitions potentially allow it to participate more directly in lending economics through co-lending, merchant finance and balance-sheet partnerships, according to an executive at a fintech startup. If executed well, that could materially improve monetisation over time.

But it also fundamentally changes the company’s risk profile. The future challenge will no longer simply be acquiring users or processing payments. It will involve capital access, underwriting discipline, regulatory execution and sustainable balance-sheet management.

MobiKwik is no longer simply trying to grow payments. It is trying to escape the paradox of payments in the Indian fintech space, which has been well documented in the past.

The company increasingly appears to understand that UPI has transformed consumer payments into low-yield infrastructure rails where scale alone no longer guarantees meaningful monetisation. That is why the future thesis is shifting toward merchant finance, lending and regulated financial infrastructure.

The business has recovered from stress, but its economics remain well below earlier levels.

The problem is that this transition remains unfinished. Payments monetisation continues weakening, merchant investments are still loss-making, and the lending business, while healthier, remains well below its earlier scale.

The next few years will therefore determine whether MobiKwik successfully reinvents itself into a broader credit-led fintech platform or remains trapped as a high-volume, low-monetisation payments utility.

MARKETS WATCH: NEW ISSUES, POST-IPO JOURNEY & MOREZaggle’s Margin Gains: Zaggle reported a strong Q4 FY26 with revenue rising 50% YoY to ₹617.9 Cr and profit increasing 30% to ₹40.6 Cr, driven by growth across Propel, program fees, and enterprise spends.

Veefin’s Profit Surge: Veefin Solutions reported a strong Q4 FY26 with revenue rising 27% sequentially to ₹131.3 Cr and profit more than doubling to ₹16 Cr, aided by expansion across its fintech SaaS stack.

Matrimony’s Slow Growth: Matrimony reported a steady Q4 FY26 with revenue rising 7.8% YoY to ₹116.8 Cr and profit increasing 18.3% to ₹9.7 Cr, aided by controlled expenses and lower marketing spends. The company also announced a dividend of ₹5 per share despite muted annual revenue growth.

Shadowfax In The Black: Shadowfax turned profitable in Q4 FY26, posting a net profit of ₹55.8 Cr against a loss last year, while revenue surged 74% YoY to ₹1,237 Cr. Growth was driven by strong express delivery volumes, rising market share in third-party logistics, and improved EBITDA margins.

Flipkart Delays IPO: Flipkart has reportedly deferred its IPO plans till at least 2028 as parent Walmart pushes the ecommerce giant to achieve EBITDA breakeven in FY27.

TAC’s Crypto Drag: TAC Infosec reported a strong H2 FY26 with revenue rising 54% YoY to ₹27.8 Cr and profit increasing 30% to ₹10.8 Cr, driven by growth in its cybersecurity and Web3 businesses. However, sequential profit declined amid higher expenses and crypto fair-value losses linked to its subsidiary Cyberscope.

The post Can MobiKwik’s Lending Ambitions Ease The Payments Burden? appeared first on Inc42 Media.

-

Mateus Mane’s Rise: From Bench to Breakthrough at Wolves Amid Interest from Manchester United and Liverpool

-

Rising to Greatness: How Barcelona’s Sydney Schertenleib Became Women’s Football’s Brightest Young Star

-

Chelsea’s WSL Reign Unravels: How Sonia Bompastor’s Risky Approach Backfired and What Lies Ahead for the Blues

-

Lionel Messi reacts to Inter Miami fans’ protest over players’ ‘respect’ concerns during MLS victory against Portland Timbers

-

Mario Basler: The Bayern Munich Maverick Whose Talent and Rebellious Spirit Defined an Era